Questions

Single choice

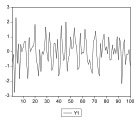

Based on the following graph, which of the following is true?

Options

A.While we cannot say for certain, the series appears to be covariance stationary

B.The series is not covariance stationary because of obvious trending

C.The series is not covariance stationary because of obvious seasonality

D.The series is not covariance stationary because of excessive volatility

View Explanation

Verified Answer

Please login to view

Step-by-Step Analysis

To assess covariance stationarity, we examine whether the mean, variance, and autocovariance are time-invariant.

Option 1: 'While we cannot say for certain, the series appears to be covariance stationary' This hedges on uncertainty, but the presence of apparent seasonal cycles typically implies non-constant mean or a......Login to view full explanationLog in for full answers

We've collected over 50,000 authentic exam questions and detailed explanations from around the globe. Log in now and get instant access to the answers!

Similar Questions

Would it be convenient to use a machine learning model directly on the time series below? I No, because the level of the time series is too high, going beyond 4000. II No, because the time window of the time series is too wide. III No, it would be better to test for the non-stationarity of the time series and transform it before applying any model. IV Yes, machine learning can deal with any type of time series without problems.

What is the primary characteristic of a stationary time series?

How would you characterize such a time series :

A random walk process (no drift!) has mean zero, that's why it's weakly stationary but not strong (strict) stationary

More Practical Tools for Students Powered by AI Study Helper

Making Your Study Simpler

Join us and instantly unlock extensive past papers & exclusive solutions to get a head start on your studies!