Questions

AP Economics-Hillebrand AP Microeconomics Sem 1 Exam 2025 - Requires Respondus LockDown Browser

Single choice

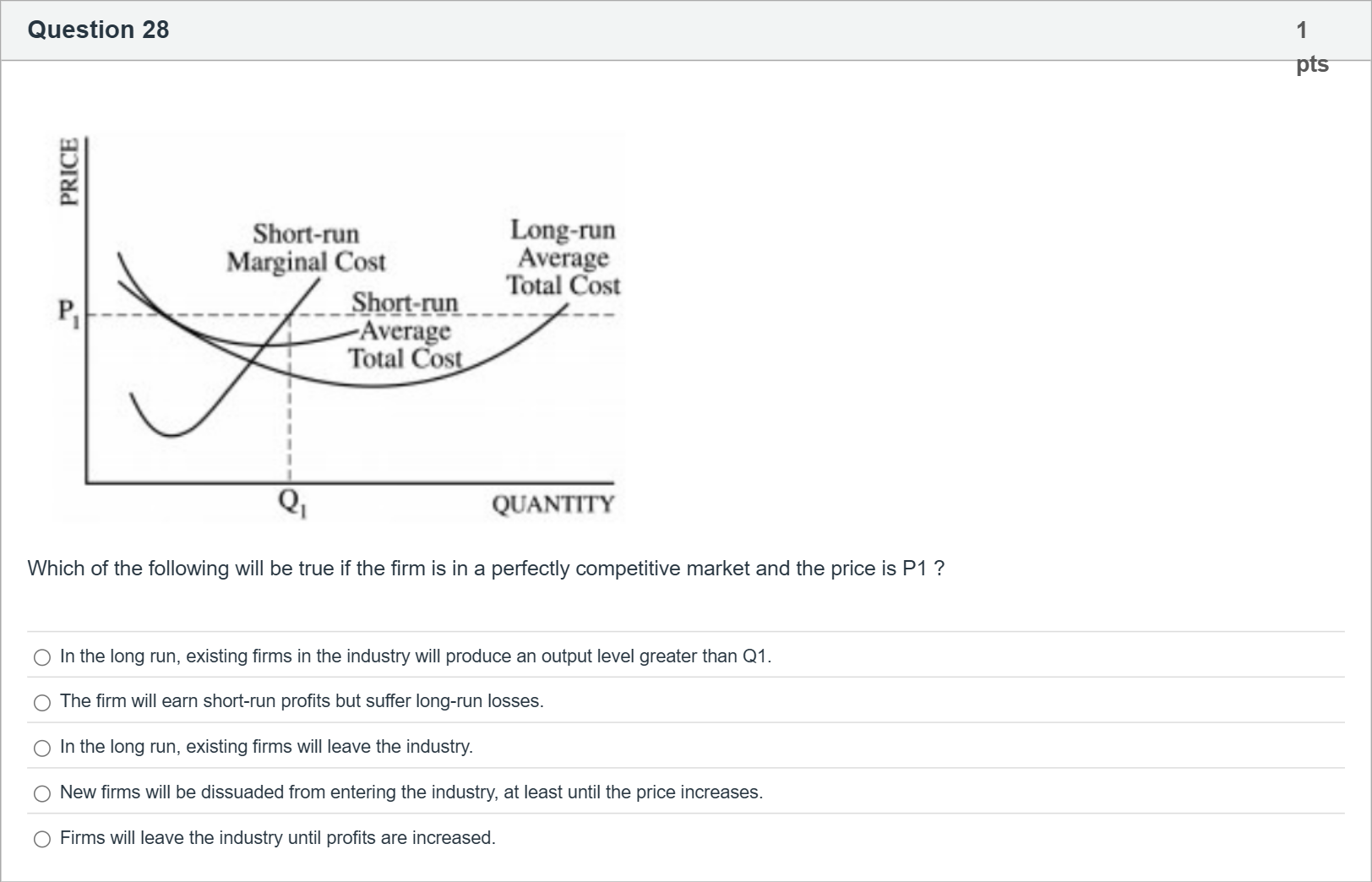

Which of the following will be true if the firm is in a perfectly competitive market and the price is P1 ?

Options

A.In the long run, existing firms in the industry will produce an output level greater than Q1.

B.The firm will earn short-run profits but suffer long-run losses.

C.In the long run, existing firms will leave the industry.

D.New firms will be dissuaded from entering the industry, at least until the price increases.

E.Firms will leave the industry until profits are increased.

View Explanation

Verified Answer

Please login to view

Step-by-Step Analysis

To begin, let's restate the question and all answer options to set the stage for analysis.

Question: Which of the following will be true if the firm is in a perfectly competitive market and the price is P1?

Options:

1) In the long run, existing firms in the industry will produce an output level greater than Q1.

2) The firm will earn short-run profits but suffer long-run losses.

3) In the long run, existing firms will leave the industry.

4) New firms will be dissuaded from entering the industry, at least until the price increases.

5) Firms will leave the industry until profits are increased.

Now, evaluate each option carefully:

Option 1: In the long run, existing firms in the industry will produce an output level greater than Q1. In perfect competition with free entry and exit, long-run equilibrium occurs where price equals the minimum of average total cost (P = ATC) and fir......Login to view full explanationLog in for full answers

We've collected over 50,000 authentic exam questions and detailed explanations from around the globe. Log in now and get instant access to the answers!

Similar Questions

In a perfectly competitive market ____________ determines how value created is divided between consumers and producers.

Zucchini is produced in a perfectly competitive market with a downward-sloping demand curve and an upward- sloping supply curve. Dawson Farm is a typical perfectly competitive farm that produces and sells zucchini at the equilibrium price of $1.75 per pound. Which of the following is true?

In the absence of barriers to entry, a typical firm is currently in long-run equilibrium. Assume there is an increase in the market demand for the good that the firm is producing. Which of the following will happen in the long run?

In a perfectly competitive market, the process of entry and exit will end when firms in the market:

More Practical Tools for Students Powered by AI Study Helper

Making Your Study Simpler

Join us and instantly unlock extensive past papers & exclusive solutions to get a head start on your studies!